Environmental issues are always concerned by the authorities and people. The increasing development of factories, manufacturing enterprises, discharges a lot of waste into the environment, causing serious impacts on the environment. From the above issues, the authorities are required to strengthen the control and minimize the harmful effects on the environment and people’s lives. One of the many measures applied is to pay environmental protection fees from organizations, individuals and households themselves when discharging wastewater into the environment. However, in certain cases organizations and individuals are still free of environmental protection.

On May 5, 2020 the Government issued Decree No. 53/2020/ND-CP stipulating environmental protection fee for wastewater taking effect from July 1, 2020. Accordingly, this Decree provides for cases of free environmental protection for wastewater. As follows:

Free domestic wastewater in 3 cases:

Domestic wastewater of organizations, households and individuals in communes;

Daily-life waste water of organizations, households and individuals in wards and townships without clean water supply systems;

Daily-life waste water of households and individuals not doing business in wards and townships already having clean water supply systems and using water by themselves.

In addition, this Decree stipulates a number of other cases that are free of charge:

Water discharged from hydroelectric plants;

Seawater used to produce salt is discharged;

Cooling water (in accordance with the law on environmental protection) is not directly in contact with pollutants and has its own outlet;

Waste water from rainwater naturally overflows;

Waste water from fishing means of fishermen;

Wastewater of centralized waste water treatment systems in urban areas is treated up to environmental standards and technical regulations as prescribed before being discharged into receiving sources.

In order to support people facing difficulties due to the impact of the Covid -19 pandemic, the State has issued many urgent measures to limit difficulties for production and business activities, ensuring social security and quality life. Accordingly, for businesses heavily affected by the Covid epidemic – 19, the Ministry of Labor – Invalids and Social Affairs issued Official Dispatch No. 1511 / LDTBXH-BHXH 2020 on guiding the temporary suspension of payment to the fund retirement and survivors on May 4, 2020.

In the Official Dispatch, it is clearly stated that, in case the Employer has to suspend production and business for 01 month or more due to difficulty in changing structure, technology or due to crisis, economic recession or to implement State policies when restructuring the economy or fulfilling international commitments; Employers who are in difficulties due to natural disasters, fires, epidemics or crop failures will be temporarily suspended to contribute to the retirement and survivorship fund.

However, the employer in the above cases may only temporarily suspend the payment to the retirement and survivorship fund when satisfying one of the following conditions:

The quantity of suspended employees who have social insurance is at least 50% of total number of employees before the suspension.

The loss caused by the natural disaster, fire, epidemic or crop failure is over 50% of total assets (excluding land);

Accordingly, the period of temporary suspension of payment to the retirement and survivorship fund for the two above cases is counted from the month the employer issues a written request but not more than 12 months.

Social insurance premiums have been fully paid by the end of January 2020 and the quantity of employees who have social insurance is decreased by at least 50% over the period from January 2020 to the date of application. The employees only includes those who have indefinite-term employment contracts, fixed-term employment contracts, employment contracts with a term of from 1 to less than 12 months; hired managers of enterprises and cooperatives. In this case, the period of temporary suspension of payment to the retirement and survivorship fund is calculated from the month the employer issues a written request and does not exceed the time limit of June or December 2020.

At the end of the suspension period, the employer and the employee continue to contribute to the retirement and survivorship fund and at the same time make compensation for the suspension period (for both employees stopped paying wages), The amount of compensation payment is not subject to late payment interest. If, during this period, the employee is eligible for retirement, survivorship or termination of the labor contract, the employer shall make payment to compensate for the suspension period. regime for employees. The provisions of this Official Letter will officially take effect from May 4, 2020.

On April 9, 2020 the Government issued Decree No.46/2020/ND-CP, effective from 1/6/2020 providing regulations on customs procedures, customs inspection and supervision of goods. transit through the ASEAN customs transit system to implement Protocol 7 on the customs transit system

Protocol 7 on the Customs Transit System was developed with the overall goal of simplifying and harmonizing regulations on movement, trade and customs; establish an effective, optimal and integrated transit system in ASEAN.

This Decree details the goods in transit through the ACTS system. Can understand the ACTS system as follows: “ACTS” means the integrated information technology system developed by Member States of ASEAN for the purposes of connecting and exchanging information to carry out electronic transit procedure, control the movement of goods across the territory of Contracting Parties, assisting customs authorities of Contracting Parties in calculating customs duties and guarantee amounts, and exchanging information for recovery of customs debts under Protocol 7 on Customs Transit System (hereinafter referred to as “Protocol 7”

The transit of goods through the ACTS system must comply with the following provisions:

1. Goods placed under the ACTS procedure which are transported from Vietnam across the territory of a Contracting Party must comply with the provisions on management of goods in transit of that Contracting Party.

2. Goods placed under the ACTS procedure which are transported across the territory of a Contracting Party and imported to Vietnam must comply with the provisions on management of goods in transit of that Contracting Party and the relevant provisions on management of imports of Vietnam.

3. Goods placed under the ACTS procedure which are transported across the territory of Vietnam must comply with the provisions on management of goods in transit laid down in relevant laws.

4. Based on the result of classification of customs declarations on the ACTS and provided information relating to the goods in transit (if any), Directors of Customs Sub-departments shall decide to carry out the examination of customs dossiers and/or the physical inspection of goods. The physical inspection of goods shall be carried out with machinery and other technical devices. If the Customs Sub-department does not have sufficient machinery and technical devices or the inspection of goods by using machinery and technical devices is not sufficient for determining the actual conditions of goods or any violations are suspected, the customs officials shall carry out the physical inspection of goods.

5. Charges which may be incurred in Vietnam in respect of goods placed under the ACTS procedure shall be paid in accordance with regulations of the law on fees and charges.

In addition, this Decree prescribes the priority regime for enterprises conducting goods transit through the ACTS System such as:

1. Free many journeys

2. Exemption from the requirement to present the TAD and the goods at the customs authority, except for the case of the ACTS failure.

3. Exemption from the examination of customs dossiers and physical inspection of goods at the customs authority of departure, except for the cases of suspected violations.

4. Use of the special seal approved by the customs authority.

5. The validity period of authorisations shall be 36 months from the date of issue of the decision on recognition of authorized transit trader status.

Decree No. 46/2020/ND-CP was issued, contributing to creating a legal basis for implementing the application of customs modernization for goods in transit between ASEAN countries and Vietnam, while contributing to reducing spending fees and facilitate businesses in the transit of goods between Vietnam and ASEAN member countries, ensuring the requirements of administrative procedure reform and customs modernization.

On May 25th, 2020, the Government issued Decree 57/2020/ND-CP amending and supplementing a number of articles of Decree No.122/2016/ND-CP dated September 1st, 2016 of the Government on the Export tax, preferential import tariff, list of goods and absolute tax rates, mixed tariffs, and non-quota import tax and Decree No. 125/2017/ND-CP dated November 16th, 2017 amending and supplementing a number of articles of Decree No.122/2016/ND-CP.

Accordingly, the preferential import tax rates for raw materials, supplies and components for production, processing (assembly) of industrial products support development priority for the automobile manufacturing and assembly industry. the period from 2020 to 2024 (hereinafter referred to as the preferential program for automobile industry tax) is prescribed as follows:

– Preferential import tax rate of 0% for domestically unavailable raw materials, supplies and components for production, processing (assembly) of products aided by development priorities for manufacturing industry, automobile assembly (hereinafter referred to as automobile supporting products).

a) At the time of registration of the declaration, the declarant shall declare and calculate tax on imported raw materials, supplies and components at the normal import tax rates or preferential import tax rates. Preferential import tax rates or special preferential import tax rates as prescribed, the tax rate of 0% has not yet been applied.

b) The application of the preferential import tax rate of 0% to raw materials, supplies and components of the automobile industry tax incentives program shall comply with the following principles:

(i) Ensuring the right subjects of application: Enterprises manufacturing, processing (assembling) automobile components and spare parts; Enterprises manufacturing and assembling automobiles produce and assemble automobiles by themselves (assemble).

(ii) Ensure the Applicable Conditions

(iii) Guarantee for the tax incentive review period: The tax incentive review period must not exceed 6 months from January 1 to June 30 or from July 1 to December 31 every year.

(iv) Ensuring sufficient documents and procedures for registering to participate in the Preferential tax program for automobile industry

(v) Implement customs declaration procedures in accordance with the law

(vi) Manufacturing, processing (assembling) establishments of enterprises participating in the automotive tax incentives program must meet the conditions prescribed by law.

(vii) Provide complete documents and carry out procedures to apply the preferential tax rate of 0%

The State Bank of Vietnam has just issued Decision 920/QĐ-NHNN on the maximum short-term loan interest rate in Vietnam dong as prescribed in Clause 2, Article 13 of Circular 39/2016/TT-NHNN of December 30th, 2016. 2016 and takes effect from the date of signing, and this Decision also replaces Decision 420/QĐ-NHNN issued by the State Bank of Vietnam on March 16th, 2020.

Accordingly, the regulation on interest rates for short-term loans are as follows:

Credit institutions and foreign bank branches (except people’s credit funds and microfinance institutions) shall offer short-term loans in Vietnam Dong with the maximum interest rate of 5.0%/year (0.5% / year lower than before)

People’s credit funds and microfinance institutions shall offer short-term loans in Vietnam Dong with the maximum interest rate of 6.0%/year (0.5% / year lower than before)

The interest rate applicable to credit contracts and loan agreements signed before May 13th, 2020 is continued to be implemented according to signed contracts and agreements in accordance with the provisions of law at the time of signing.

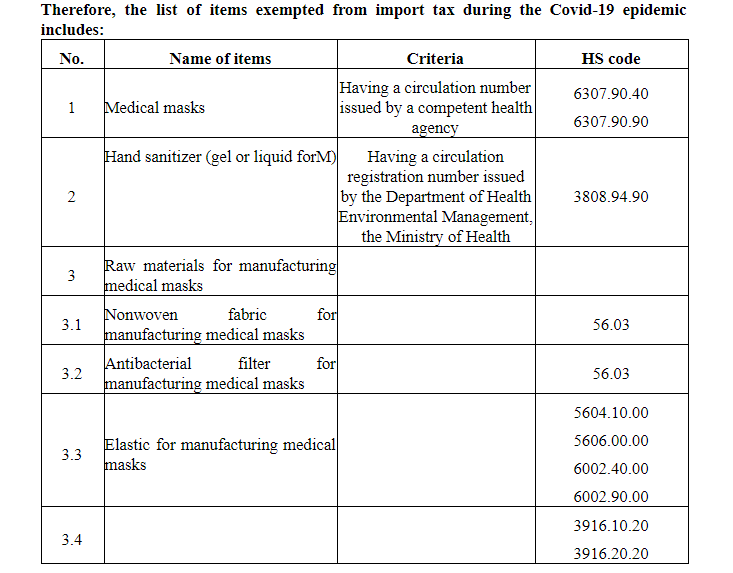

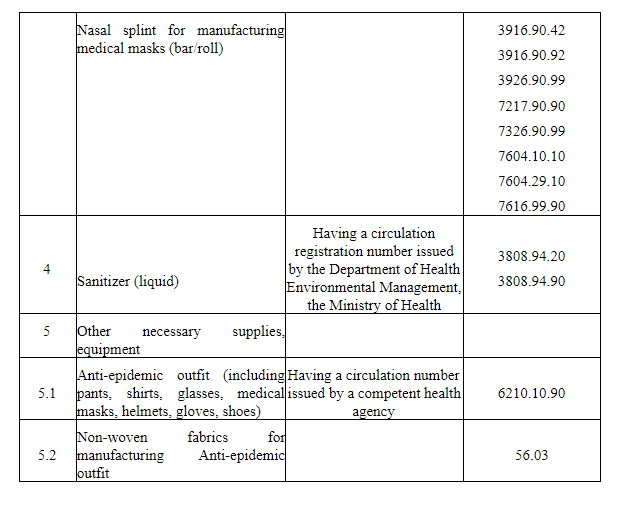

On February 7, 2020, the Prime Minister issued Official Letter No. 197/TTg-KTTH of exempting import tax on medical masks and hand sanitizer; raw materials for the production of masks, antiseptic water, necessary supplies and equipment in service of the prevention and control of acute respiratory infections caused by corona virus.

On February 7, 2020, the Ministry of Finance issued Decision No. 155/QD-BTC on the list of items exempted from import tax for the prevention and control of acute respiratory infections caused by corona virus.

On March 27, 2020, the Ministry of Finance issued Decision No. 436/QD-BTC to supplement items exempted from import tax to the list in the previous Decision No. 155/QD-BTC.

Document No. 2698/BCT-DTĐL was issued on April 16, 2020 by the Ministry of Industry and Trade on supporting electricity price reduction for customers using electricity affected by Covid epidemic -19.

According to the Decision No. 648/QD-BCT issued on March 20, 2019, the average retail price of electricity is 1,864.44 vnđ/KWh (excluding VAT). With the complicated situation of the Covid 19 epidemic, which has seriously affected the socio-economic life of Vietnam, the Ministry of Industry and Trade has sent a written request to the Department of Industry and Trade of the provinces and cities directly. of the Central Government and Vietnam Electricity Group shall apply the policy of reducing electricity sale prices and reducing electricity charges to individuals and organizations, specifically as follows:

1. Price reduction:

– 10% reduction will apply to the retail rates for commercial customers and industrial customers in Decision No. 648/QD-BCT dated March 20, 2019 for peak, shoulder and off-peak periods.

– 10% reduction will apply to retail rates of level 1 to 4 for residential customers in Decision No. 648/QD-BCT.

– Retail rates for industrial customers will apply to tourist accommodation establishments (according to the 2017’s Law on Tourism and relevant laws) instead of commercial rates.

– Wholesale rates in rural areas, dormitories or residential clusters; wholesale rates for commercial-residential complexes: 10% reduction will apply to residential rates of level 1 to 4; 10% reduction will apply to wholesaling of electricity for other purposes according to Decision No. 648/QD-BCT.

– Wholesale rates for industrial zones and markets: 10% reduction will apply to the wholesaling tariff in Decision No. 648/QD-BCT.

2. Discounts (before tax) for EVN’s customers that participating in Covid-19 control:

– 100% discount will be given to quarantine facilities other than hotels, treatment facilities for suspected cases and confirmed cases of Covid-19.

– 20% discount will be given to health facilities where suspected cases and confirmed cases of Covid-19are examined, tested and treated.

– 20% discount will be given to hotels that are used for quarantine of suspected cases and confirmed cases of Covid-19.

The list of facilities eligible for discounts shall be provided for electricity supply units by National Steering Committee for Covid-19 Control, the Ministry of National Defense, the Ministry of Public Security and the People’s Committees of provinces.

This policy has contributed to reducing financial stress for individuals and businesses, for manufacturing businesses with high demand for electricity, the reduction of electricity prices helps these businesses accumulate costs. contribute to the recovery of business after the disease situation stabilizes

Solar power is a new group of energy industries developed recently in Vietnam. Most solar power projects are concentrated in localities such as Ninh Thuan, Gia Lai, bac Giang, Hai Phong… The development of solar power is receiving many policies to encourage and support the state.

On April 6, 2020, the Prime Minister issued Decision No. 13/2020/QD-TTg on the mechanism to encourage development of solar power in Vietnam, effective on May 22, 2020. Accordingly, organizations and individuals participating in the development of solar power in Vietnam will be applied the new electricity tariff as prescribed in this Decision.

Decision No. 13/2020/QD-TTg has specified the lower power purchase price, the discount price than the old price. All three types of solar power connectors, ground sun and solar power roofs have the same price level, namely the following:

For power projects floating Solar: 1,783 VND/kWh, equivalent to 7.69 UScent/kWh;

For the ground solar power project: 1,644 VND/kWh, equivalent to 7.09 UScent/kWh;

For solar power system roof: 1,943 VND/kWh, equivalent to 8.38 UScent/kWh.

Some outstanding issues when applying the above electricity tariff, businesses should pay attention, specifically:

For electricity projects Grid-connected solar power projects have been decided by competent agencies on investment policies. before November 23, 2019 and have a commercial operation date of the project or part of the project from July 1, 2019 to the end of December 31, 2020, that project or part of that project may be The electricity buying tariff of grid-connected solar power projects shall be applied as above.

For Ninh Thuan province, the purchase price of electricity from grid-connected solar power projects is included in the electricity development planning at all levels and has the date of commercial operation before January 1, 2021 with the total accumulated capacity of zero. exceeding 2,000 MW is VND 2,086 / kWh (exclusive of value-added tax, equivalent to 9.35 UScents / kWh, at the central rate of Vietnam dong and US dollar announced by the State Bank of Vietnam). April 10, 2017 was VND 22,316 / USD), applied for 20 years from the date of commercial operation.

For rooftop solar power systems, it is permitted to sell part or all of the electricity produced to the Buyer being Vietnam Electricity Group or the purchaser is another organization or individual in case of not using the electricity grid. of Vietnam Electricity. Vietnam Electricity Corporation or its authorized member unit shall make payment of the electricity from the rooftop solar power system to the national grid at the above purchase price. This purchase price is applied to rooftop solar power system with the time of generating electricity operation and certification of meter readings from July 1, 2019 to December 31, 2020 and is applied. Use 20 years from the date of commissioning.

In order to implement the Prime Minister’s directing opinions in Document No. 2827/VPCP-KTTH of April 10, 2020 on rice export in the context of epidemics, drought and saltwater intrusion. On April 10, 2020, the Ministry of Industry and Trade issued Decision 1106/QD-BCT announcing export quotas for rice in April 2020 (“Decision 1106 / QD- BCT”).

The main contents of Decision 1106/QD-BCT:

Export quotas for rice: The rice export quota (HS code 10.06) applied in April 2020 is 400,000 tons.

Principles of quota management:

Traders who register the previous customs declaration will be deducted from the previous export quota. The quantity declared on the registered customs declaration will be subtracted from the amount permitted for export in April. In case the customs declaration is no longer valid for carrying out the procedures or the actual export quantity is less than the declared quantity, the overage will be added back to the amount permitted for export in April.

Customs declarations are valid for carrying out customs procedures until the total number of export registrations of declarations reaches 400,000 tons (customs declarations with an amount in excess of 400,000 tons will not be valid for customs procedures). In case the customs declaration is no longer valid for carrying out procedures or the actual export quantity is less than the customs declaration amount, the overage will be added back to the amount permitted for export in April.

Export border gates: Only rice exports are allowed through international border gates (road, rail, sea, waterway and air).

Exceptions:

Exporting rice to supply ships on exit (serving the daily life of sailors on board not exceeding 30kg / 1 sailor). export processing enterprises

On-spot import and export or export to export-processing enterprises (serving activities of employees in export-processing enterprises).

Decision 1106/QD-BCT takes effect from 0h April 11, 2020.